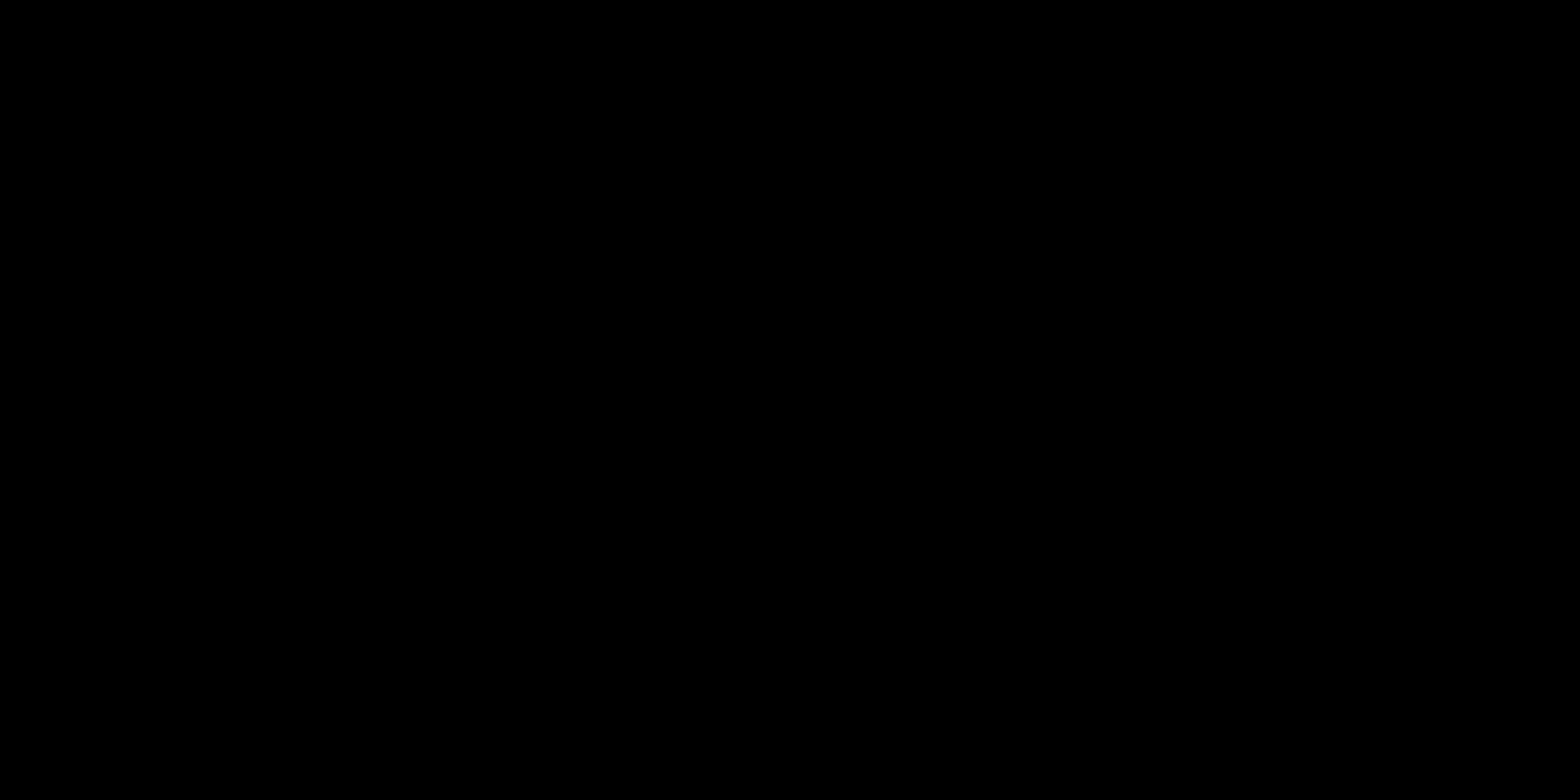

What is exposure tracking in the USA?

Exposure tracking is knowing, state by state, where your business has (or is about to have) a sales-tax obligation. The US has no national sales tax: each state sets its own rules, and you pick up an obligation either by selling enough into a state (economic nexus) or by having people, inventory, or property there (physical nexus).

For a growing company that exposure shifts constantly: a new warehouse, a remote hire, or a single large order can cross a threshold. Commenda tracks all 50 states in real time so a new obligation never catches you off guard.

The two types of nexus

Sales-tax nexus comes in two forms, and either one on its own creates an obligation:

- Economic nexus is triggered purely by crossing a state's revenue or transaction threshold (commonly $100,000 in sales or 200 transactions), even with no presence in the state. Established by the 2018 South Dakota v. Wayfair decision.

- Physical nexus is triggered by a physical connection to the state: employees or contractors, an office, inventory (including 3PL and FBA stock), owned property, and in some states traveling reps, trade-show attendance, or affiliate and click-through arrangements.

Use the toggle on the map above to switch between the two views. The sections below go deeper on economic nexus and how each state measures it.

What is economic nexus?

Economic nexus is the link between your business and a state that obligates you to register, collect sales tax, and file returns there. Unlike physical nexus (established by an office, warehouse, employee, or inventory), economic nexus is triggered purely by crossing a revenue or transaction threshold.

Every state with a statewide sales tax has enacted an economic nexus law. The specific threshold, what counts toward it, and how often it is evaluated differs by state.

Why economic nexus matters for remote sellers

Before the 2018 Supreme Court decision in South Dakota v. Wayfair, Inc., a state could only require a business to collect sales tax if it had a physical presence in the state. The Wayfair ruling allowed states to base nexus on economic activity alone, opening the door for every state to require remote sellers - including e-commerce, SaaS, and digital goods businesses - to collect tax once they cross a threshold.

The financial stakes are significant. Failing to register after crossing a threshold can result in back taxes, interest, and penalties stretching back years. A growing business can easily trigger nexus in 20 or more states in a single year without realizing it.

How thresholds are measured

Thresholds fall into four categories, and each state uses one of them:

- Sales only - registration is required once gross sales into the state exceed the dollar threshold (most common).

- Sales or transactions - crossing either limit triggers nexus.

- Sales and transactions - both limits must be exceeded for nexus to attach (Connecticut and New York).

- Transactions only - rare; no current state uses this as a sole basis.

The measurement period also varies. Some states evaluate the prior calendar year, some look at the current or previous calendar year, and a handful use a rolling 12-month window measured quarterly.

What counts toward the threshold?

This is where the rules diverge most sharply between states. Common variations:

- Exempt sales - included in most states, excluded in a few. A wholesale-heavy business can hit the threshold without owing any tax.

- Marketplace facilitator sales - excluded in most states (because the marketplace remits the tax), but a handful still include them.

- Services and digital goods - treatment varies. SaaS, electronically-delivered software, and digital products are taxable in a growing number of states.

- Sales for resale - generally excluded but not universally.

The detail expanders in the state list below show exactly what each state counts.

What creates physical nexus?

Physical nexus is the older, pre-Wayfair standard: a tangible connection to a state. Unlike economic nexus, there is no dollar threshold; a single qualifying presence is enough to require you to register, collect, and remit. Essentially every state with a sales tax asserts it, so the question is rarely whether a presence counts, but which of your activities create one. The most common triggers:

- People in the state: employees, contractors, or sales reps who live in or travel to the state, including remote hires.

- Offices and locations: any owned or leased property, such as an office, store, branch, or a home office used for the business.

- Inventory and warehouses: stock held in the state, including goods in a third-party (3PL) warehouse or an Amazon FBA fulfillment center. A trigger many sellers miss.

- Temporary presence: trade shows, conferences, or traveling staff. Some states set a day or dollar threshold; others count a single event.

- Affiliate and click-through nexus: relationships with in-state affiliates or referral partners who drive sales to you, treated by some states as a form of physical presence.

Because physical presence sticks, some states also apply trailing nexus, an obligation that continues for a period after the presence ends. Once any of these applies, the registration and filing requirements are the same as for economic nexus.

States with no statewide sales tax

The following states do not impose a statewide sales tax, so there is no economic nexus to track at the state level:

- Delaware

- Montana

- New Hampshire

- Oregon

Alaska has no state-level sales tax, but local jurisdictions in the Alaska Remote Seller Sales Tax Commission enforce a $100,000 economic nexus threshold - so Alaska is included in the state list below.